Not Just Another EV Story

How Electrifying Public Fleets is Disrupting India’s Traditional Bus Duopoly

One of the largest sources of FDI into India over the past decade has been foreign private equity capital flowing into infrastructure assets, a trend that was institutionalised with the launch of the National Monetisation Pipeline (NMP) by NITI Aayog. The programme aimed to unlock value from brownfield public infrastructure and successfully monetised government assets worth over ₹5.3 lakh crore between FY22 and FY25.

Think of roads, power, and mining, foreign PE funds like KKR invested over $3 Bn between 2019 and 2024, further strengthening their commitment through long-annuity vehicles like the Asia Infrastructure Funds, which allocate up to ~30% to Indian infrastructure assets.

But what happens when the KKRs of the world get interested in e-buses as a category to bet big on in India? Investors who have historically deployed capital into 20–25 year assets such as roads and renewable energy are now looking to bet on the segment. This signals that institutional capital is ready to back India’s EV adoption story.

This is where we are focusing on in our today’s write up.

State of Indian Cities

Indian cities are among the world’s most congested urban centres. The tech-jungle of Bengaluru has come out as the table-topper within Indian cities and the 2nd most congested city worldwide, preceded only by Mexico City. Annually, commuters in Bengaluru lose a whopping 168 hours roughly stuck in traffic, a duration equivalent to an entire work week. Pune comes in 2nd within Indian cities, sitting at the 5th spot globally for congestion, followed by Mumbai, New Delhi, Kolkata, Jaipur and Chennai.

On other side, an analysis by the Centre for Research on Energy and Clean Air (CREA) has found that about 44% Indian cities face chronic air pollution.

“Out of 4,041, at least 1,787 cities exceeded the national annual PM2.5 standard every year across five recent years (2019-2024, ex of Covid year of 2020)”

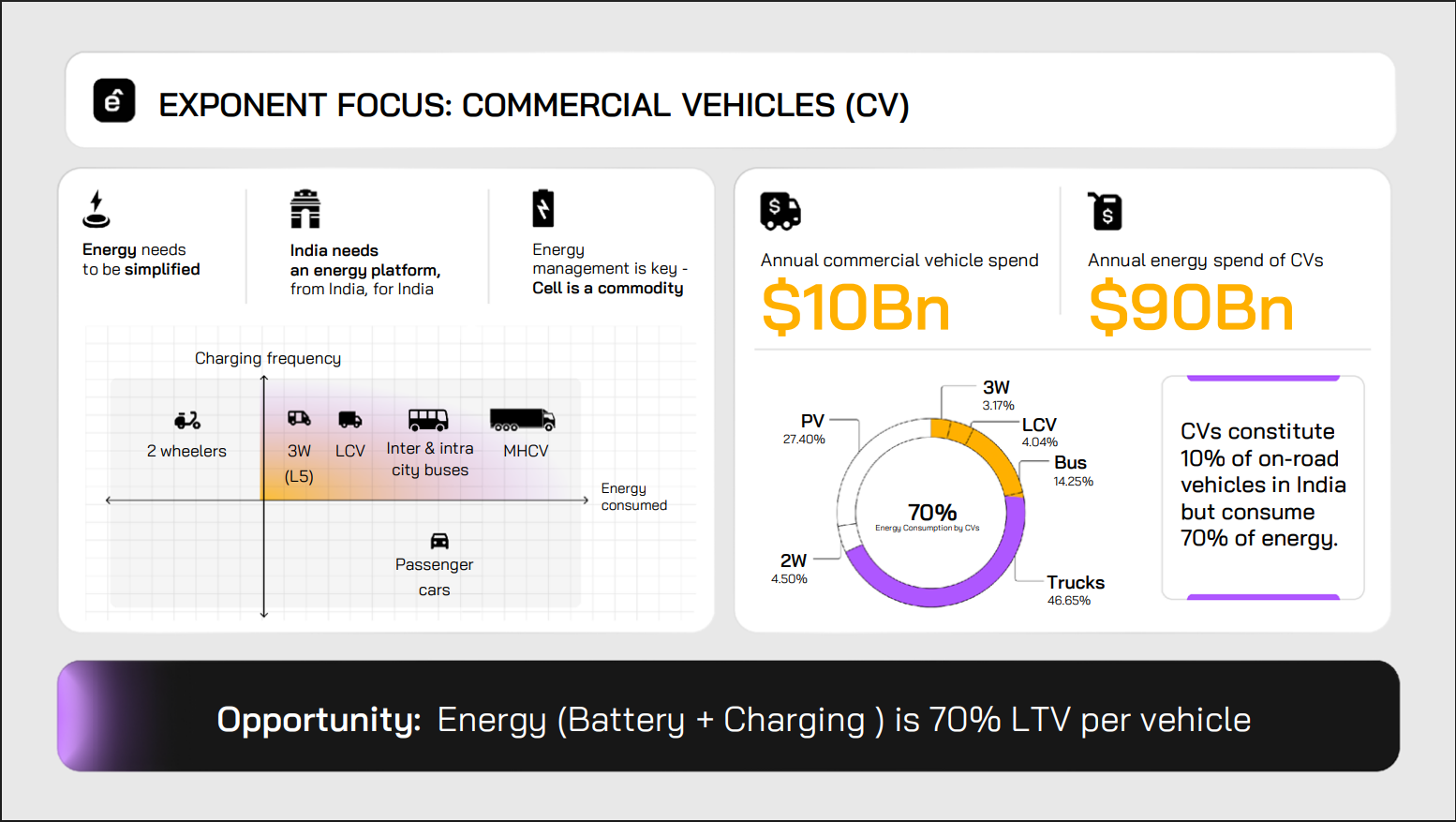

Commercial vehicles (CVs), including buses, account for nearly 70% of vehicular pollution in India, despite making up only ~10% of the total vehicle fleet, reflecting their disproportionately high share of on-road fuel consumption. In total, nearly $90 Bn is spent annually on energy to run the CV fleet alone.

Lost productivity from traffic converges with rising healthcare costs, lower labour efficiency and declining quality of life. In effect, India’s urban growth model is beginning to impose a dual tax on its residents: time lost on the road and years lost to polluted air.

Congestion on this scale cannot just be solved by widening roads or building more flyovers. Indian cities require high-frequency, reliable and well-prioritised public transport systems, which has not kept pace with urbanisation. Hence the most rational starting point for policymakers is the electrification is high-utilisation public fleets. Buses run predictable routes, clock significantly higher daily kilometres than private vehicles and operate in dense corridors where pollution exposure is the highest.

India already has ~18 lakh buses on the road, most of them diesel-powered, with state transport undertakings collectively losing ₹15,000-20,000 crore annually, driven by volatile fuel costs and import dependence. The traditional solution has been to build metro systems, but at ~₹400 crore per kilometre and long gestation periods, they are inherently limited in scale. India has over 800 cities that need mass transit. Metro can serve a handful. Electric buses can scale across all.

Policy-Driven Adoption Curve

The e-bus story is structurally different from other EV segments. Unlike passenger cars or two-wheeler, where adoption depends on consumer sentiment and retail affordability, e-buses are driven by institutional procurement and public policy design. In effect, the states are the anchor customer operating via GCC model.

Gross Cost Contract (GCC) model in bus tenders involves the operator owning and running the buses while the government pays a fixed per-km fee, retaining control over routes, fares and revenue.

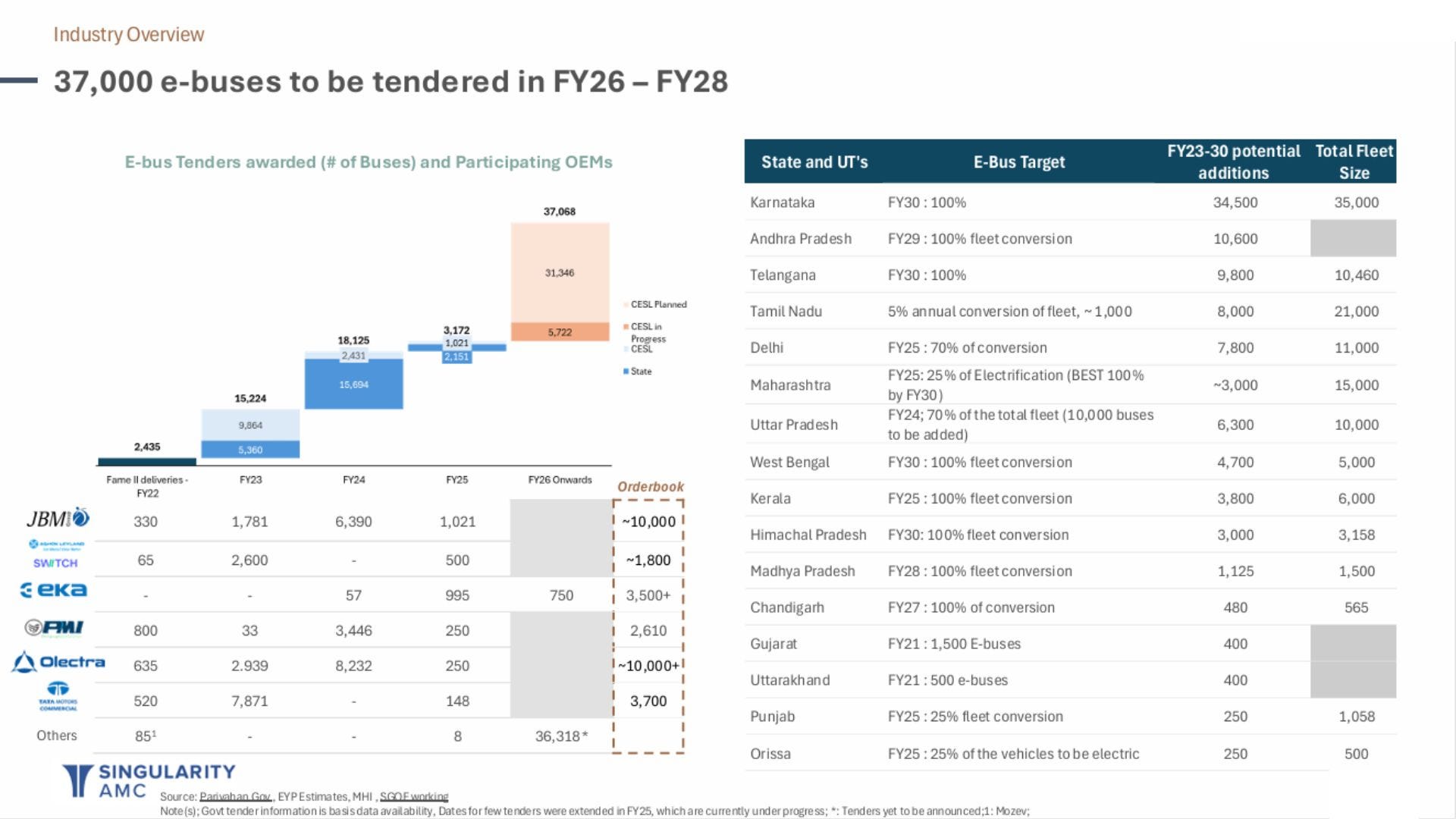

Maharashtra for example has set a 2037 deadline for an all-electric state bus fleet, aiming to convert its entire fleet of around 22,000 buses to electric vehicles (EVs), from the current base of only 800 buses. (source)

Similarly, the Central government has committed an estimated ₹67,000 Cr across FAME II, PM e-Bus Sewa, PM e-DRIVE and related schemes, effectively turning electrification from a pilot initiative into a funded, multi-year capex cycle.

The economic case underpinning this policy push is equally compelling. India has nearly 20 lakh buses on the road, the mostly still diesel-powered, while state transport undertakings collectively incur annual losses of ₹15,000-20,000 crore. Over a 12-year lifecycle, an e-bus with roughly ₹80 lakh upfront cost and ₹8 per km operating expense delivering a total cost of ownership of about ₹1.65 crore, compared to nearly ₹3.5 crore for a diesel bus, translating into savings of ~₹1.8 crore per vehicle. With standard government contracts assuming 180 km daily utilisation, break-even can be achieved in roughly 3 years.

As a result, adoption appears to be at an inflection point, with broad-based scale-up now in sight. The bus segment is likely to lead this transition, driven by high utilisation economics and institutional demand, further supported by CESL (Convergence Energy Services Ltd), which is emerging as a central demand aggregator and program manager, helping lower procurement costs for state transport undertakings and accelerating adoption.

Disruption of the Duopoly

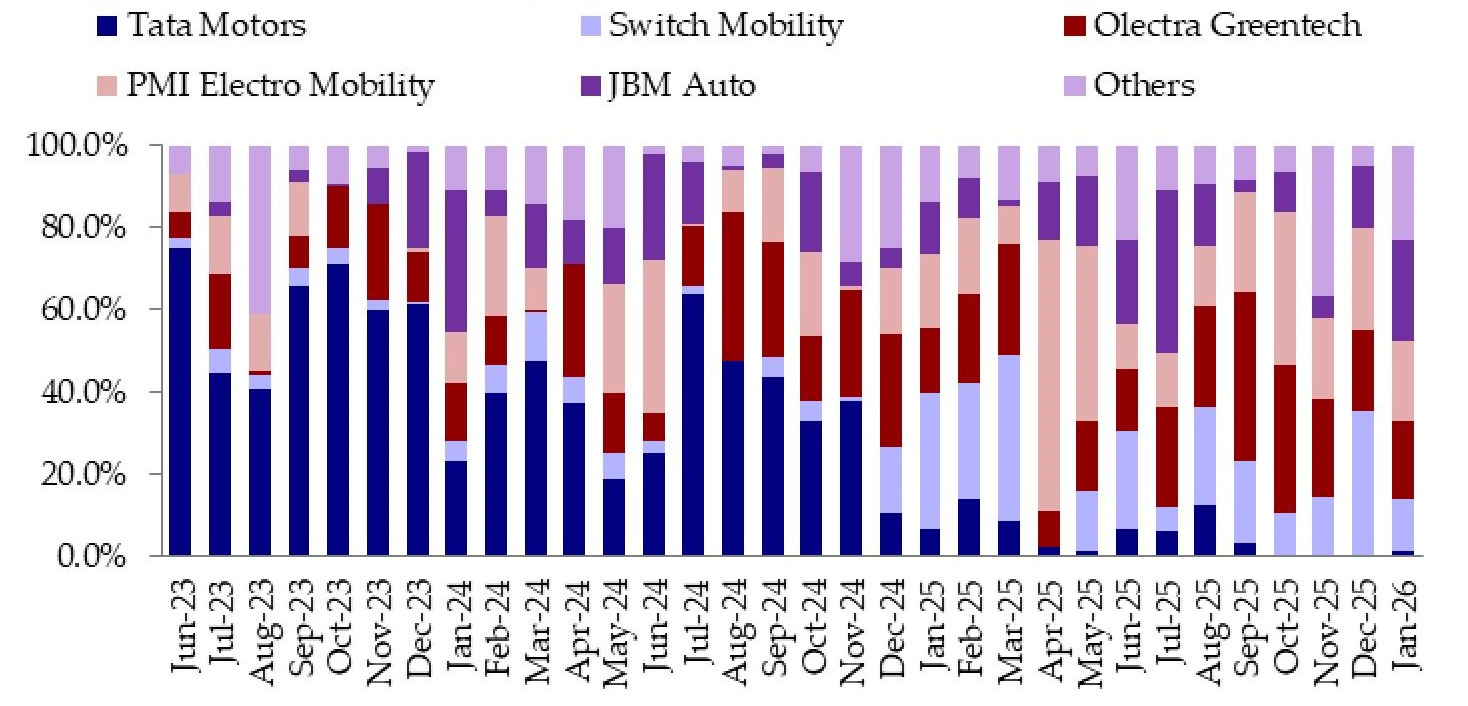

But this electrification of India's public transport has precipitated a rare structural disruption in the automotive sector, altering the competitive dynamics of the bus segment. Unlike the internal combustion engine (ICE) bus market, which has historically been a duopoly dominated by Tata Motors and Ashok Leyland, the e-bus segment has witnessed the aggressive ascent of new entrants. As of recent years, market leadership has shifted toward a consolidated group of focused electric players including Olectra Greentech, PMI Electro Mobility, JBM Auto who collectively command a majority share of the market today.

This trend stands in stark contrast to the electric 2-wheeler, 3-wheeler and passenger vehicle (PV) segments, where incumbents like TVS, Bajaj, and Tata Motors have successfully leveraged their brand equity and distribution power to retain dominance.

Given that the primary customer is the State Transport Undertaking (STU) operating under the GCC model, the traditional automotive playbook of ‘sales and service’ through dealer networks becomes largely irrelevant. The market has effectively shifted from a product-led retail model to a contract-driven, service-oriented business. This B2G (Business-to-Government) structure prioritizes best bidders (L1 tenders) where Challenger OEMs have moved faster than legacy players and now control the market leadership.

Learning Global, Building Local

E-buses are not inherently difficult to electrify, especially relative to smaller vehicle segments where space constraints are binding. The real challenge lies in optimising for commercial duty cycles. These vehicles are expected to run 250-600 km daily on fixed routes, requiring careful calibration of battery size, range, charging strategy and overall vehicle efficiency within tight operating economics.

At the same time, India’s battery ecosystem, which remains the largest cost component of the vehicle, is still evolving with a heavy reliance on imported lithium-ion cells. Challenger OEMs therefore took a lead on this front. They actively entered into early partnerships with Chinese players to get quality batteries imported. PMI Electro Mobility partnered with Foton in 2017 an technology assistance agreement including access to their platform & supply chain backbone. Olectra leveraged its deep technical collaboration with BYD to deploy proven their Blade battery rather than experiment from scratch. These alliances helped them compress their learning curve, followed by push for localization.

Partner → Learn → Localise → Own

Foton’s imported inputs accounted for a majority of PMI’s cost of goods in FY24, which has since reduced significantly in FY25 as localisation has progressed. Battery packs, motors and software are now increasingly assembled in-house, lowering import dependence. This transition has also supported margin expansion, with gross margins improving by a few hundred basis points alongside operating leverage.

Capital Follows Conviction

Next leg of this transition is being underwritten by private capital.

As referred to at the start, KKR is investing up to $310 Mn through a partnership with PMI Electro Mobility and its e-bus platform, Allfleet India, acquiring a majority stake in the platform. Allfleet serves as PMI’s dedicated e-bus platform, focused on building, owning and operating large-scale electric public transport fleets and is on track to deploy over 5,000 e-buses under long-term concession & service agreements with multiple state transport authorities, supporting urban mobility across key Indian cities.

In our view, this is a clear signal that new-age players have reached a level of scale & execution maturity where global private equity is willing to underwrite the opportunity.

From City to Highway

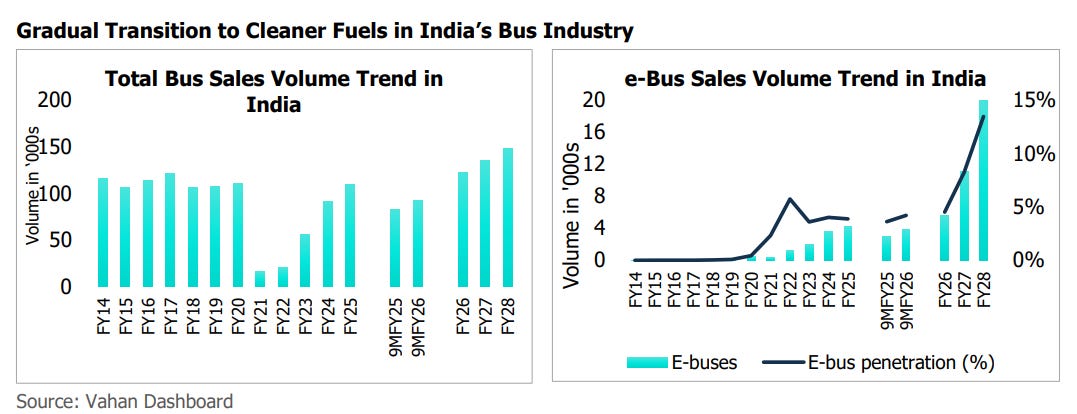

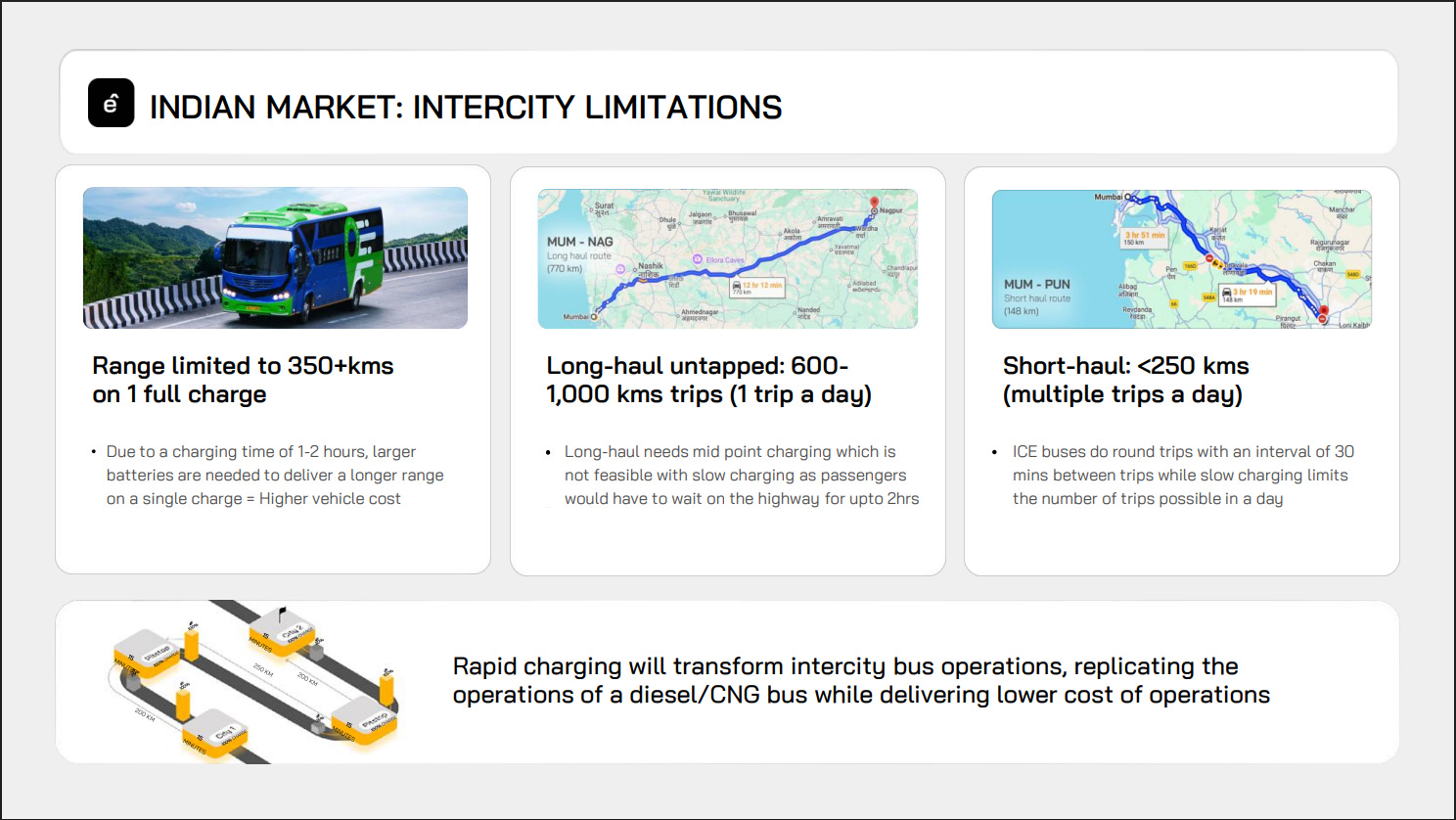

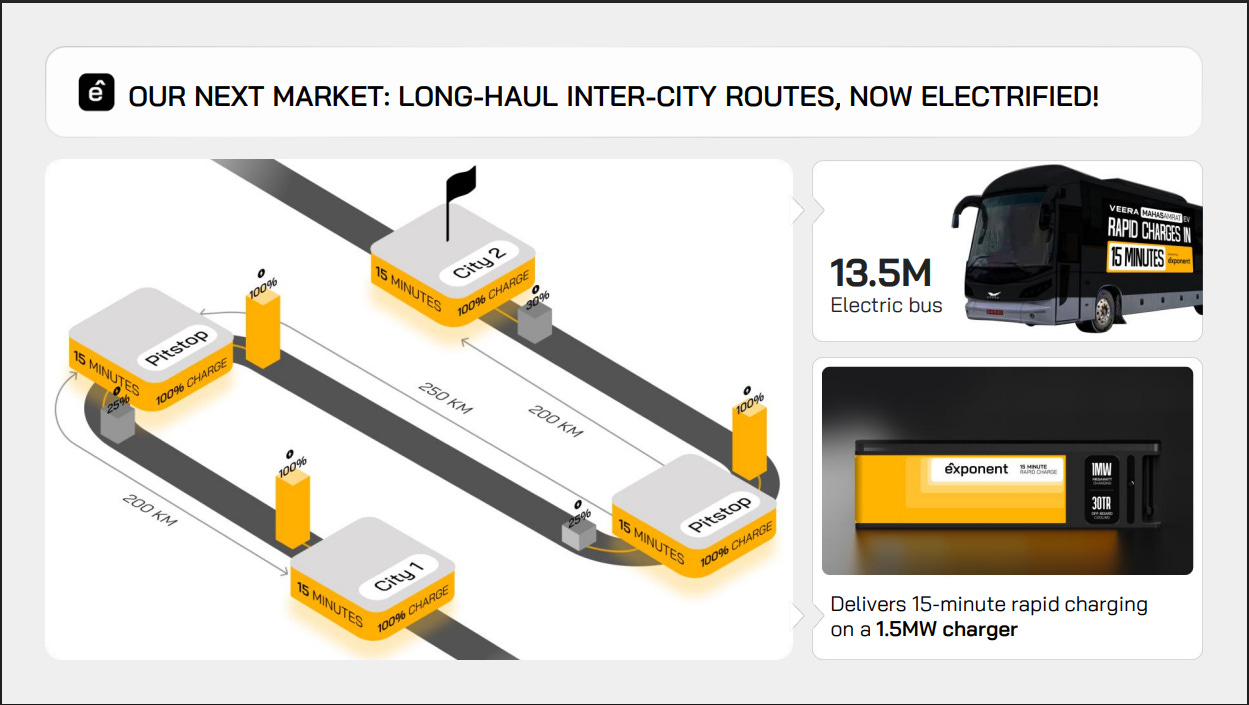

Roads carry nearly 90% of passenger traffic in India, and with the national highway network expanding ~60% between 2014 and 2025, intercity mobility is becoming faster, denser and more relevant. The overall bus segment is expected to grow at a steady 4-6% CAGR over FY25-30, making it one of the largest and most scalable mobility categories in the country.

Yet, electrification in buses today remains largely an intra-city story. Most e-buses offer a real-world range of ~300-350 km per charge, which makes them well-suited for urban routes but constrains long-haul intercity operations that typically span 600-1,000 km per trip. Mid-point charging remains a bottleneck, as long dwell times are operationally unviable for scheduled passenger services. Even in short-haul intercity routes (<250 km), charging turnaround impacts fleet utilisation versus diesel alternatives. This is why intercity remains under penetrated today as relevant infrastructure is still catching up.

With roll out of high-speed charging corridors has the potential to unlock intercity e-bus operations at scale, enabling faster turnaround times and replicating diesel-like utilisation with lower operating costs. As charging infrastructure evolves, intercity could emerge as the next major demand pool.

Diesel buses have historically delivered a poor user experience, being noisy, polluting and unreliable, which pushed the middle class toward personal vehicles and set off a negative cycle of rising congestion and worsening air quality. Electric buses change that equation. They are quieter, smoother and more accessible with low-floor designs, while also offering more predictable up time due to far fewer moving parts.

This improvement in experience can drive higher ridership, which in turn supports denser route networks and gradually reduces dependence on personal vehicles, creating a self-reinforcing cycle that diesel buses were never able to trigger.

To Conclude

E-bus opportunity in India is no longer just an EV adoption story, but the emergence of a new infrastructure asset class. It is anchored in structural demand, backed by policy, and increasingly underwritten by long-duration capital seeking predictable cash flows. Unlike other EV segments driven by consumer behaviour, this is a contract-led, economics-driven transition that is already moving toward scale.

Diesel is structurally expensive, polluting and inefficient, while e-buses offer a clear cost advantage over life cycle, alongside better reliability and user experience. With intra-city adoption already scaling and intercity poised to unlock next as charging infrastructure evolves, the addressable opportunity remains significantly under-penetrated.

In that sense, the question is no longer whether India will electrify its bus fleet, but how quickly this transition scales and which players are best positioned to execute in a capital-intensive, operations-led market.

Read more about EVs adoption in our recently blog:

This is an exceptional industrial breakdown. Shifting the electrification thesis from consumer garages to public transit depots hits the absolute core of how we must model sub-regional public finance and localized voter volatility.

Historically, municipal transport undertakings (STUs) have been structural fiscal black holes for state governments, requiring permanent, heavy budgetary bailouts that exhaust the fiscal headroom of regional administrations.

On substack.com/@electoralindex, we run demographic survey raking to track how execution velocity alters voter sentiment. When states deploy Gross Cost Contract (GCC) models for e-buses, they effectively convert massive, volatile capital expenditure into smooth, predictable operational outlays. This newly unlocked municipal fiscal cushion directly finances targeted urban welfare buffers—compressing the standard polling variance in dense urban assembly seats that traditional tracking frameworks routinely miss.