Strategic Autonomy: India’s Blueprint for Resilient Growth

Podcast: Yash Kela (Founder & CIO, Singularity AMC) with Sonia Shenoy

In the globalised world we live in today, countries depend on each other for oil & gas, semiconductors, defence equipment, critical minerals, medicines, and technology platforms. This interdependence works fine until geopolitics intervenes. In India’s case, during the 1991 crisis, when oil prices rose and widened our deficit, and we were left with barely 2 weeks of foreign exchange for imports, the country was forced to airlift 67 tonnes of gold to the Bank of England and the Bank of Japan as collateral to secure a bailout. When there is a lockdown in China or critical mineral supplies are cut off, our automobile sector, which supports over 30 million jobs, is impacted. Our dependence on energy imports is also weaponized through higher tariffs imposed by other nations, hurting our sectors such as textiles, gems and jewellery, and aquaculture.

This is where Strategic Autonomy comes into the picture, with one motto: we will trade with the world, but we won’t let the world control our survival. It sits between two extremes:

Total Globalisation which brings efficiency but also high vulnerability when geopolitics or supply chains break down, and

Isolation, which reduces dependence but hurts competitiveness & growth.

For India, the answer lies in taking this balanced path, staying integrated with the world while building enough domestic strength and diversification to minimise strategic risk. At Singularity AMC, this is not just a macro observation for us. It is the core organising principle of how we invest.

We believe when a country with India’s scale moves from 80-90% import dependence to even 40-50% localisation in critical sectors, the shift is not just incremental, it creates entirely new profit pools, new industrial champions, and new export capabilities.

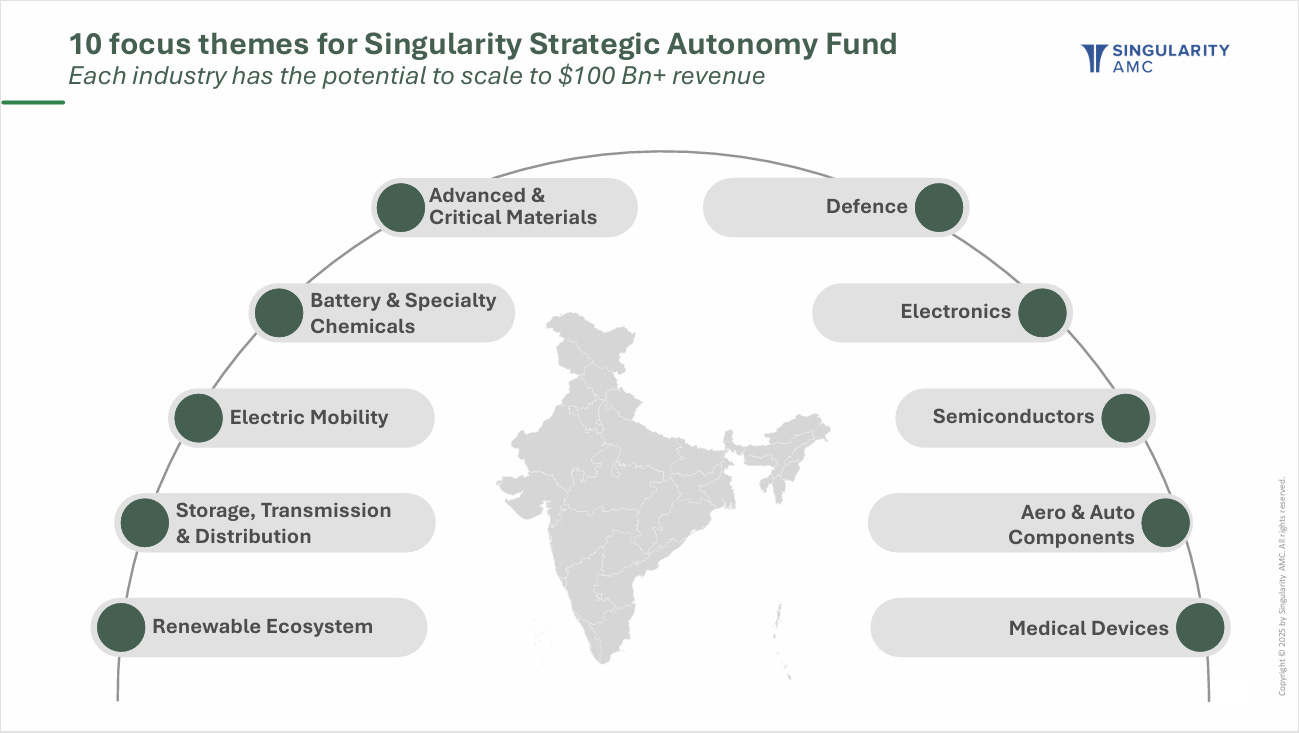

Our aim is to identify sectors where three forces converge:

Clear national intent: Whether it is PLI incentives in electronics, ECMS support for PCBs, ISM backing semiconductors, or the 75% domestic reservation in defence capex, the direction of capital formation is unmistakable.

Structural import gaps: In electronics, we consume roughly $150 Bn but add only ~20% value domestically. In semiconductors, we consume ~$50 Bn and produce less than 10%. In defence, indigenisation lists now cover over 4,000 components that must be sourced locally. These are not small substitution opportunities but multi-billion-dollar revenue pools waiting to be built.

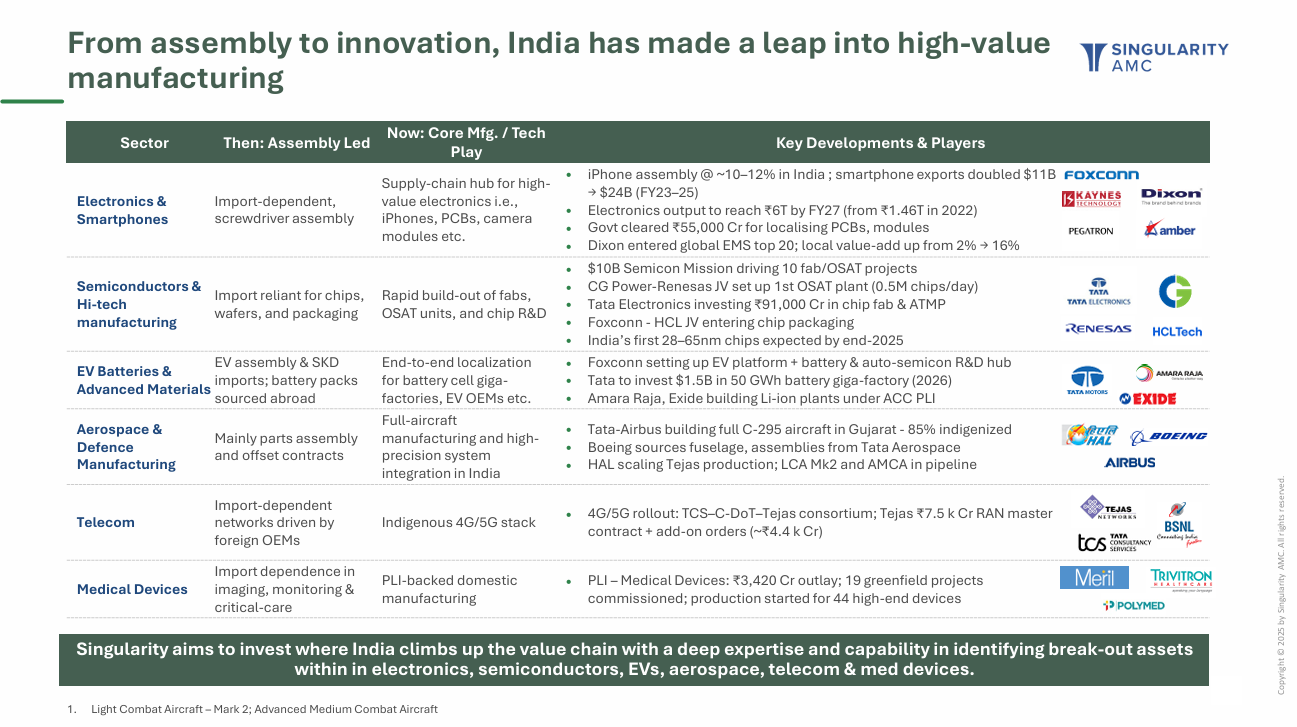

Execution capability: Strategic autonomy only works when policy meets entrepreneurial execution. We look for companies that are moving upstream, absorbing technology through partnerships, improving unit economics through incentives, and building export competitiveness. Businesses that shift from assembly to components, from platforms to electronics, from low-margin manufacturing to IP-led systems.

2nd Order Effect: Road to Become Product Nation

Countries that lack strategic autonomy become vulnerable during geopolitical tensions, supply chain disruptions, or sanctions, limiting their ability to act purely in their own interest. Whereas, countries that build around it gain control over essential value chains, strengthen their negotiating power, and attract long-term capital. Over time, this shift does more than reduce risk, it transforms them into EXPORT POWERHOUSE.

Let’s take the example of India’s defence exports, which were just around ₹700 Cr in FY2014. Government policies then evolved, and DAP 2020 (Defence Acquisition Procedure) was introduced, giving clear preference to the procurement of high-quality equipment manufactured in India. The bar was set high, and today 75% of our defence spending happens on ‘Made in India’ products.

The bigger benefit comes in the form of a second-order effect, wherein increased participation by private firms and a prospering ecosystem helped India export a record ₹23,622 Cr in FY 2025. We are now looking at ₹50,000 Cr of exports by 2029.

So the need of Aatmanirbharta has actually shown us the path of prosperity, huge employment opportunities by becoming a PRODUCT NATION. Similar is the case of electronics where while the domestic manufacturing grew 6X in the last 11 years, the exports actually grew 8X and continue to grow much faster with increasing value addition. This unlock continues to take place across the sectors we are focused on.

Road to Viksit Bharat 2047

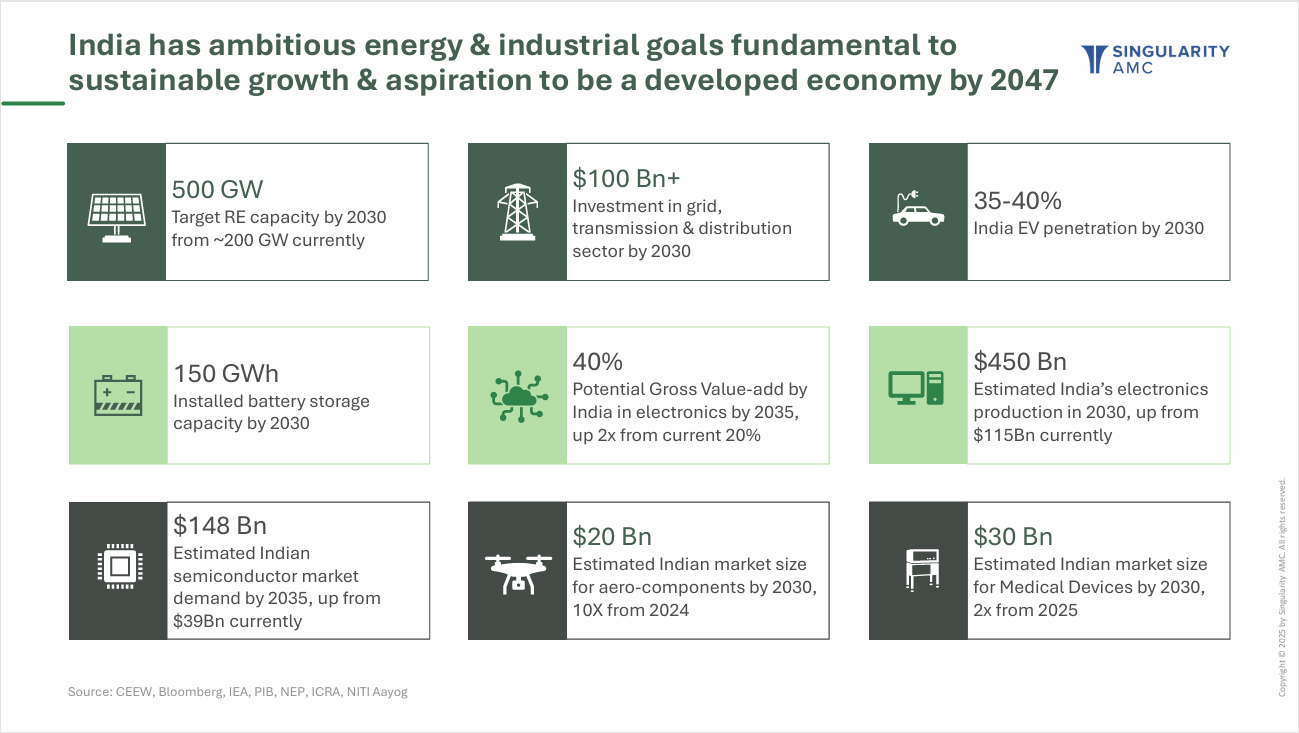

India’s ambition to become a developed economy by 2047 is anchored in a massive industrial and energy expansion over the next decade. The country is targeting 500 GW of renewable energy capacity by 2030, alongside $100 Bn+ of investments in grid and transmission infrastructure. EV penetration is expected to reach 35-40% by 2030, supported by 150 GWh of battery storage capacity. On the manufacturing side, electronics production is projected to scale from $115 Bn today to $450 Bn by 2030, while semiconductor demand could rise from $39 Bn currently to $148 Bn by 2035. Defence production stands at roughly ₹1.5 lakh crore annually, with exports already touching ₹23,622 crore in FY25 and a target of ₹50,000 crore by FY29. These are not isolated sectoral ambitions. They represent the foundation of a new industrial architecture.

Viksit Bharat 2047, therefore, is a capital cycle story. Energy security, electronics depth, semiconductor capability and defence indigenisation together create compounding industrial capacity. India’s path over the next 20 years will likely be defined by how effectively it converts today’s import gaps into tomorrow’s global competitiveness.

As these structural changes continue to play out across our sectors of interest, we at Singularity AMC are here to accelerate that shift.

We recently discussed this framework in greater depth in a podcast conversation between Yash Kela and Sonia Shenoy, where the idea of Strategic Autonomy was unpacked from both a national and investment lens. The discussion centred on a simple but powerful shift: moving from assembly-led participation in global supply chains to owning deeper layers of capability, whether in electronics, defence systems, energy infrastructure or advanced manufacturing.

A key takeaway from that conversation was that strategic autonomy is not about isolation, but actually building enough domestic strength to negotiate with the world from a position of confidence. For investors, that translates into identifying businesses that are genuinely moving up the value chain, strengthening technology depth, and creating optionality beyond policy incentives. If you would like to explore the thinking behind this theme in more detail, you can watch the full conversation below.

Watch the full podcast:

$1B Investor’s Guide to India’s Next Boom: Defence, EVs & Solar

Check out our latest posts below:

Mastering the Modern Influencer Playbook

The Investor Operator Playbook: From Face to Founder, How mCaffeine Combined Authenticity with Execution

AI Goes Vertical in Financial Services

Deep Dive: Intelligence Layer Cutting Across Banking, Lending, Insurance & Payments